13. October 2021 By Dennis Hensch

Barriers to digitalisation in the reinsurance sector

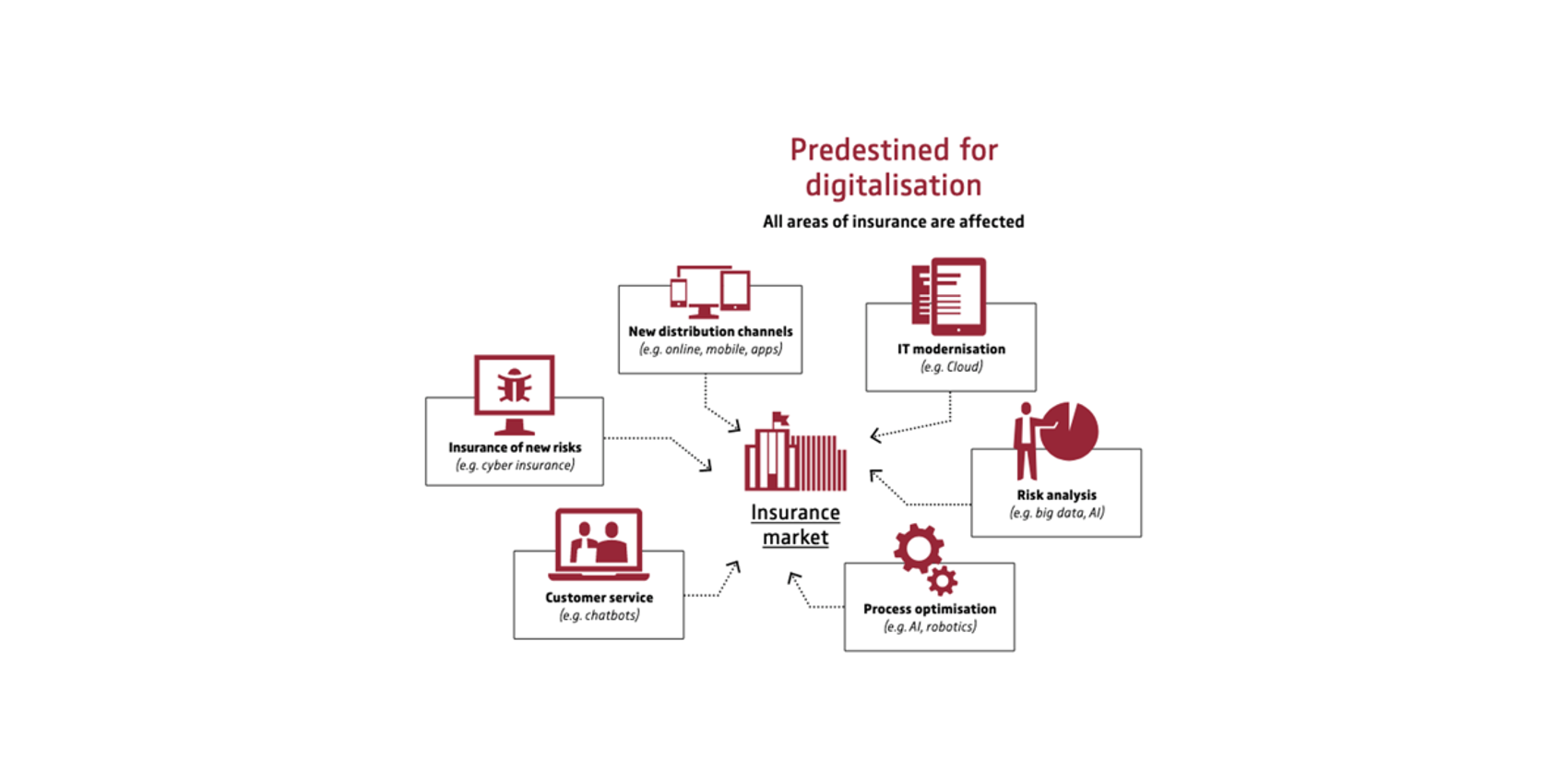

Barriers to digitalisation in the reinsurance sector – fact or fiction? Because ‘digitalisation’ is broadly interpreted in the insurance sector, it’s a bit of both.

According to their definition, digitalisation includes processes that are converted from analogue to digital, digital interfaces to customers, sales partners and service providers as well as new business models and services.

Digitalisation is more complex than most people think. Buzzwords like artificial intelligence (AI), big data, distributed ledgers, blockchain and hybrid customers along with the associated tools like customer relationship management (CRM) systems and content management systems (CMS) are hot topics at the moment.

Source:GDV: The Positions of German Insurers in 2020, https://www.en.gdv.de/resource/blob/57388/9fcc93c45b8fd70a866436cbffd54c5b/publikation---die-positionen-der-deutschen-versicherer-2020-data.pdf

Is that also the case with reinsurers?

There have always been certain unique features of the reinsurance business that set it apart from other sectors and make it particularly interesting.

Reinsurance is generally understood to be insurance for insurance companies. Why, then, should there be barriers at reinsurers if the relevant insurance and reinsurance experts underwrite similar types of business?

- Reinsurers continue to generate strong business and profits. As a result, they may not currently feel the pressure to invest in ‘digitalisation’. But this could prove to be a competitive disadvantage for what are now the ‘larger’ reinsurers going forward if the ‘smaller’ reinsurers are now in the process of establishing future digitalisation strategies that work best for their companies.

- Unlike primary insurers, there is no one single calculation basis used by all reinsurers. The calculations produced by actuaries who assess the risks and portfolios are done behind closed doors using proprietary methods. The main goal, even today, is to understand the business and establish the calculation basis, even for risks that were previously not insured by anyone or were even deemed ‘uninsurable’. This is achieved by having the necessary experience, exercising due diligence and validating risks.

The top-five reinsurers often serve in a pioneering role in the development of methods for calculating an expected loss value, which other reinsurers then follow or accept.

Underwriting expertise therefore continues to play a central role in the market positioning of reinsurance companies today.

- Reinsurers assess individual risks and do not handle volume business, which is why it is often difficult to develop digital processes. Describing the distinctive features and exceptions is often an extremely time-intensive undertaking. They are typically still performed manually or using non-automated processes.

- For many reinsurers, evaluating fully structured data and having a higher-quality database containing this information are two factors that are playing an increasingly important role.

The main challenge here is the heterogeneous IT landscape of primary insurers, with its vast array of interfaces and data formats.

Structured data is often not available, while central pool data and downstream data science (extracting insights and defining fields of action) are still very fragmentary or incomplete.

- Since reinsurers are not only active on the German market, this is something that must be considered and implemented with a view to international collaboration with local units on markets in other countries. The various national and legal frameworks, along with the (regional) accounting requirements that have to be taken into account, tie up resources at reinsurers or are incomplete. The Eastern Europe and Asia region, in particular, continues to be highly attractive for reinsurers since it perceived to be a lucrative market due to the higher growth potential there.

- There is evidence that the top-three reinsurers have a clear advantage in terms of expertise in mortality data: They have gained vast experience with data analytics over the past few years. In this area, the smaller reinsurers are trying to catch up quickly.

We’re now done with the overview of the various trends and barriers to digitalisation.

German insurers IT spending for the first time over EUR 5 five billion in 2019

I would have liked to list and compare the investments made to date by insurers and reinsurers, but GDV only publishes the IT cost ratios of primary insurers.

The IT spending of German insurers rose by 15% y-o-y, to EUR 5.5 billion in 2019, the German Insurers Association (GDV) said. The boost provided by the pandemic to digitization will probably result in even higher expenses, but also in changed priorities in the digitalization journey.

The IT expense ratio, which is calculated from IT costs in relation to gross premium income, also rose significantly. While its value stood at 2.17% in 2017, 2.3% in 2018, and was of 2.5% a year later, according to the annual IT survey of the German Insurance Association (GDV). In absolute terms, this increase meant a plus of EUR 800 million in 2019 vs. 2018.

Source: Daniela Ghetu for primm.com

By contrast, the IT cost ratio of reinsurers is not published at any central location that I could find.

There are only a few scattered press releases and publications on individual projects as well as the project costs listed there. A barrier to openness and transparency?

How do we plan to eliminate the barriers described above together with you to generate new opportunities?

adesso is your partner in helping you to successfully design and implement a strategy that fits your needs. Take advantage of our knowledge of the reinsurance industry and the expertise of our consultants and developers in all things related to customer-orientated solutions.

At an interaction room workshop, we work with you to identify and prioritise the strategic and operational challenges in and around digitalisation. Going from there, we can take a systematic approach to developing and visualising recommendations for the implementation at your company.

adesso has demonstrated time and again that it has the experience needed to handle highly confidential data in past work for insurers, banks and companies in other industries, including the lottery and public sectors. We have expertise in professional and technical projects, including ones involving challenges specific to waterfall and agile methods.

From a process perspective, many people today equate digitalisation with automation. In our view, however, processes are more comprehensive and far-reaching, and they do not ‘simply’ automate manual work. Implementing digital solutions and standardised mechanisms for activities that are still largely paper-based today should be the goal. When it comes to collecting, processing and using data, we support you during the data conversion and migration processes as well as in carrying out wording analyses and implementing corporate governance measures. Last but not least, the possibility of modularising additional services (Services and Support), such as earthquake maps and similar services, should be explored and subscription models (CRM models) evaluated.

To do so, we use proprietary products like KI Expert, Data Analytics, Datenmigration MiG Suite, INRelation, adesso Transformer and many more. Along with that, we also have high-profile strategic partnerships in our portfolio.

We look forward to hearing from you.

Would you like to learn more exciting topics from the (digital) insurance market at adesso?

Category: |

|

Tags: |

Insurance Customer Service Customer loyalty |